Tax Planning and the CARES Act

by Drew Overton | May 22, 2020 | Financial Planning, Retirement Planning

The Corona-virus Aid, Relief, and Economic Security (CARES) Act was signed into law on March 27, 2020. At over 800 pages long, it can be overwhelming to think about all the changes that have come from this legislation. For today, we’ll walk through different segments of the CARES Act that may impact you and what tax planning opportunities come to mind in response to these changes.

Due dates for federal income taxes have been postponed to July 15, 2020.

Per the IRS website, the due dates for both filing your federal tax return and paying any federal taxes have been pushed back to July 15, 2020. Keep in mind, there is nothing you need to do on your end—no need to file any extra forms, and no need to call the IRS. If July 15th still isn’t enough time, you can simply request an automatic extension to file your federal income tax return.

Additionally, first quarter 2020 estimated income tax payments originally due April 15, 2020, and second quarter 2020 estimated income tax payments originally due June 15, 2020, have both been postponed to July 15, 2020 (Notice 2020-23). All you need to do is make one payment of the combined amount due (the estimated tax payments for both quarters) by the July 15, 2020 deadline.

The government only offered a delay in filing and paying taxes, meaning they still want all their money. But let’s make this simple. If you are expecting a refund, go ahead and file now to receive your refund—there is no benefit in waiting. However, if you are expecting to have to pay, it could be nice to wait. Think about “spreading” the tax liability across a couple of months. By that I mean you can start saving a little in May and June so that the tax bill isn’t as painful in July—just a thought.

Quick note for VA residents (directly from the Virginia Tax website):

Individual income tax payments for Virginia are now due June 1, 2020. This change applies to payments originally due between April 1 and June 1, 2020, including:

- individual tax due payments for taxable year 2019,

- individual extension payments for taxable year 2019, and

- first estimated income tax payments for taxable year 2020.

No penalties, interest, or addition to tax will be charged if payments are made by June 1, 2020. Also, Virginia has an automatic six-month extension to file your income tax. Keep in mind, if you file during the extension period, make sure you still pay any taxes owed by June 1, 2020 to avoid penalties.

Due dates for contributions to retirement plans have also been postponed to July 15, 2020.

Contributions to IRAs and certain other retirement plans have been pushed back to the new tax filing deadline of July 15, 2020. Have you already filed your 2019 return but want to make an IRA contribution? No worries. You can simply amend your return and make the contribution for 2019.

One financial planning services idea for funding your IRA involves the new economic impact payments. As these rebate checks from the government are sent out, there are many things you can do with them. You may spend it on a new TV, use it to help purchase a new car, or even just save the money. However, as financial planners we ask the question, why not use that money to invest in your retirement? This is a great way to fund your IRA for 2019, or get a jump start on funding your IRA for 2020. Please keep in mind that the contribution limits and the income limits for deductibility still apply.

Required minimum distributions have been waived for 2020.

Required minimum distribution (RMD) rules have been waived for calendar year 2020 for IRAs and certain defined contribution plans. For people who do not need their RMD for living expenses, this provides a few high-impact financial planning services opportunities.

For example, let’s say last year you had monthly income that you used for living expenses (meaning Social Security and/or a pension) and on top of that, you took your required minimum distribution only because it was required by law. The RMD caused your taxable income to be higher and let’s assume it pushed you into a higher tax bracket.

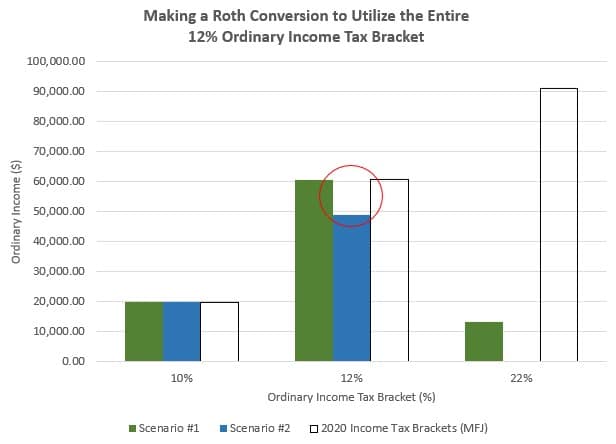

Now for 2020, that IRA distribution (the RMD) is not forced out. In this example, not taking your RMD causes you to drop into a lower tax bracket this year. The following chart below shows two hypothetical scenarios for a married couple filing jointly and taking the standard deduction in 2020. The first scenario assumes they have pension income of $75,000, social security income of $25,000, and an RMD of $25,000. The second scenario is the same as the first, except without taking the RMD.

| Scenario #1 | Scenario #2 | |

| RMD | $25,000 | $0 |

| Pension and Social Security | $100,000 | $100,000 |

| AGI | $121,250 | $96,250 |

| Standard Deduction | $27,400 | $27,400 |

| Taxable Income | $93,850 | $68,850 |

| Ordinary Income Tax Bracket | 22% | 12% |

| Projected Federal Tax Owed | $12,198 | $7,866 |

The main point of this hypothetical example is not necessarily to show the lower estimated tax bill, but rather to show the lower projected tax bracket. Now, from here some might say, “Great, sounds good. I just won’t take my RMD this year.” However, the real financial planning services opportunity lies within the tax brackets. Consider doing a Roth conversion to “use up” the 12% bracket. By converting, not only do you pay the tax within a lower tax bracket, but the amount you convert can continue to be invested within a retirement vehicle providing tax-free growth. Essentially, you could pay the tax now (most likely at a lower rate than if you withdraw it in the future), keep the funds invested, and not have pay tax upon withdrawal. Pretty impactful.

The following chart shows how your taxable income is spread across the different ordinary income tax brackets for our hypothetical example. Scenario #1 shows if you take your $25,000 RMD as normal. Scenario #2 shows if you decide not to take your RMD. As mentioned before, the main planning idea here is to do a Roth conversion for the amount that utilizes the entire 12% bracket—in this case, around $12,000 (circled in red in the chart below). By “using up” the remaining 12% bracket, the money is converted to a Roth IRA, taxed at a low rate, and can now grow tax-free for future withdrawals.

Change in limitation for charitable contribution deductions.

For the 2020 tax year, the deduction percentage limitation for charitable contributions of

cash has been removed for individual taxpayers. If you remember back to the Tax Cuts and Jobs Act of 2017, it increased the limitation for cash contributions to 60% of adjusted gross income. However, the CARES Act has now suspended the limitation entirely for cash contributions. This simply means that you can receive a deduction for gifts to qualified charities up to your adjusted gross income, and any excess contributions will be carried over. Breaking it down even further, this means that you could essentially give away your entire tax liability in 2020…paying nothing in taxes. However, please keep in mind that this change is only applicable for cash contributions, not gifts of appreciated securities or any other gifts.

For taxpayers who do not itemize their deductions, you can still receive a small deduction for qualified charitable contributions. Beginning in tax year 2020, if you take the standard deduction and gift up to $300 cash to a qualified charitable organization, you will receive an above-the-line deduction. This may not seem like a lot, but every little bit helps.

I hope this provides clarity and some insight into your 2019 and 2020 taxes. If you feel that any of the financial planning services ideas above could potentially impact you, please feel free to call our office to discuss your specific financial planning situation at (757) 436-1122.

*TFG does not provide tax, legal or accounting advice. This material has been prepared for informational purposes only, and is not intended to provide, and should not be relied on for, tax, legal or accounting advice. You should consult your own tax, legal, and accounting advisors before engaging in any transaction.